Worrying debt risk

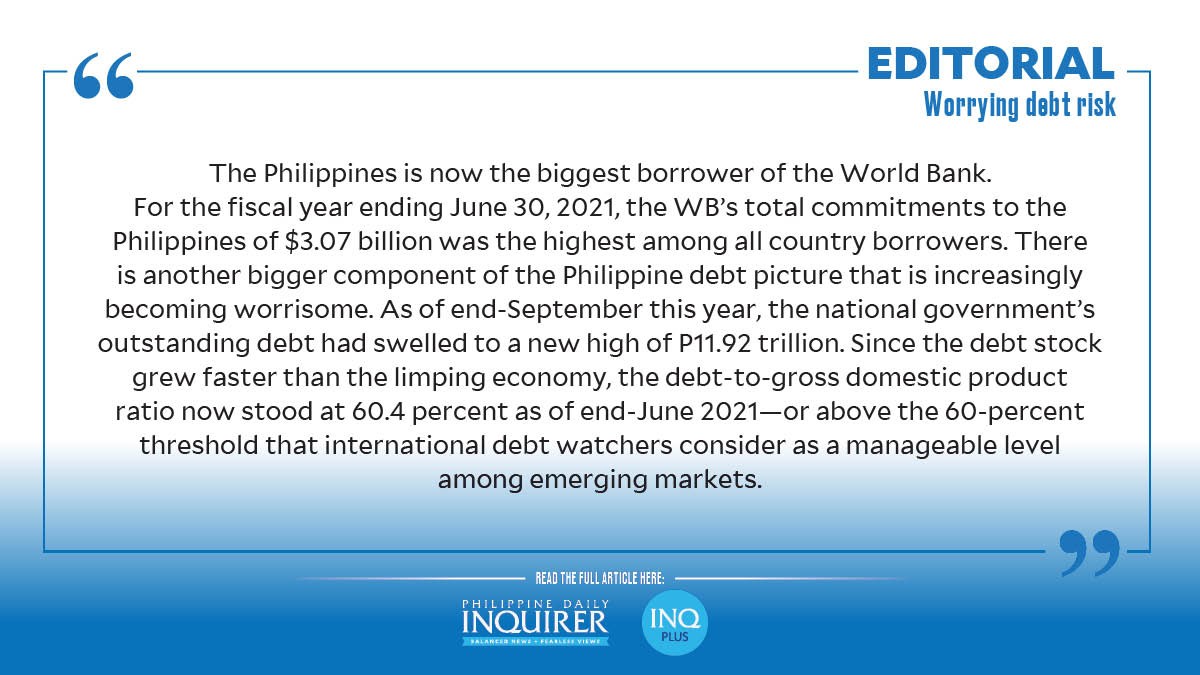

The Philippines is now the biggest borrower of the World Bank, the multilateral lender with the twin goals of ending extreme poverty and promoting sustainable prosperity. This development can be seen as beneficial in that those loans will go to financing infrastructure projects, and developmental programs in vital sectors such as education, public health, and poverty alleviation. As a bonus, the loans carry low interest rates and long repayment periods of at times exceeding 20 years.

The World Bank’s annual report for the fiscal year ending June 30, 2021 showed that its total commitments to the Philippines of $3.07 billion was the highest among all country borrowers. The World Bank reasoned that the Philippines had the biggest financing shortfall in the East Asia and Pacific region in 2020 and was thus among the countries that benefited from its fast-track facility for emergency COVID-19 response. Besides health-care and vaccine financing, the World Bank also extended loans for the Philippines’ conditional cash transfers, customs modernization, disaster resilience and recovery, peace-building in the Bangsamoro Autonomous Region in Mindanao, and various agricultural projects.

There is, however, another bigger component of the Philippine debt picture that is increasingly becoming worrisome, especially for the administration that will take over after the May 2022 elections. As of end-September this year, the national government’s outstanding debt had swelled to a new high of P11.92 trillion. It was up 27.2 percent from P9.37 trillion a year ago. Latest data from the Bureau of the Treasury showed that domestic borrowings, which accounted for 70.4 percent of the total, grew by 30.3 percent to P8.39 trillion, while foreign debts jumped by 20.4 percent to P3.53 trillion.

Since the debt stock grew faster than the limping economy, the debt-to-gross domestic product (GDP) ratio now stood at 60.4 percent as of end-June 2021—or above the 60-percent threshold that international debt watchers consider as a manageable level among emerging markets. The debt-to-GDP ratio, which reflects an economy’s ability to repay its obligations, is expected by the government to settle at 59.1 percent at the end of this year—the worst in 16 years. Before the pandemic, the debt-to-GDP ratio was at a record-low 39.6 percent in 2019.

Amid the pandemic-induced economic slump, lower revenues forced the government to borrow more from multilateral banks and foreign governments and issue debt paper here and abroad. The bulk of these expenses was triggered by the health crisis, which has had such a debilitating and lingering effect not only on the Philippines but on the global economy as well. The Department of Finance reported last September that the government secured $22.51 billion (P1.13 trillion) in foreign financing during the past year and a half just to beef up its war chest to fight the COVID-19 crisis.

President Duterte’s economic managers have pushed back at the view that the swelling debt is becoming unsustainable, arguing that it would remain manageable based on the metric of how it ranges against GDP, or the total value of goods and services produced in the economy for a given period.

The GDP, however, can easily shrink whenever unforeseen events happen; the recession in 2020 because of the pandemic is proof of that. This has been the main argument for keeping debt at more prudent levels.

The Philippines is no stranger to a debt crisis. The Marcos years in the 1970s saw the country’s debt rise due to the availability of so much “petro-dollar” loans, the excess money the oil-rich Middle East earned when crude prices soared in 1973 and 1979 and were recycled into cheap loans tapped by developing countries. At the onset of the 1980s, a debt crisis caused by Latin American borrowers failing to pay their obligations had a domino effect on the Philippines, forcing it to seek a moratorium on debt repayment. This resulted in the country entering an agreement with the IMF wherein it would lend money in exchange for an austerity program that eventually caused hardships on Filipinos.

The Duterte administration may consider the present debt level still manageable, but the options are progressively getting narrower. Nobody can predict if the pandemic will indeed be resolved soon and allow economic activity—especially travel and tourism—to recover to a decent level, let alone anywhere near pre-pandemic levels. What if a new variant of the virus that cannot be stopped by existing vaccines emerges? The Philippines cannot afford to go through the same severely constricting measures adopted in 2020 to address the crisis which tanked the economy. And it will no longer have the same borrowing capacity to finance its responses, while already trillions-deep in debt. That will be the biggest risk facing the next administration.